Before I take on a new coaching client, I let them know that there are three rules to coaching that I need them to agree to before we get started. The first and most important of these rules is that they agree to do whatever I ask them to do, even if it doesn’t make sense at the time.

Experience has taught us that you can’t half do a budget; you can’t just pick the bits that are comfortable and easy to follow and leave the bits that are time-consuming or difficult to implement.

One of the least popular expectations I have of clients is that they modify their bank account structure to support their budget. I understand that changing bank accounts is a major hassle. Finding time to get to the bank, changing all your direct debits, and organising with your employer to deposit your pay into a new bank account all takes time.

However, the request is not without good reason; it is my experience that most people seriously overcomplicate their finances by having too many bank accounts and credit cards.

How you set up and use your bank accounts plays a significant role in the success (or failure) of budgeting.

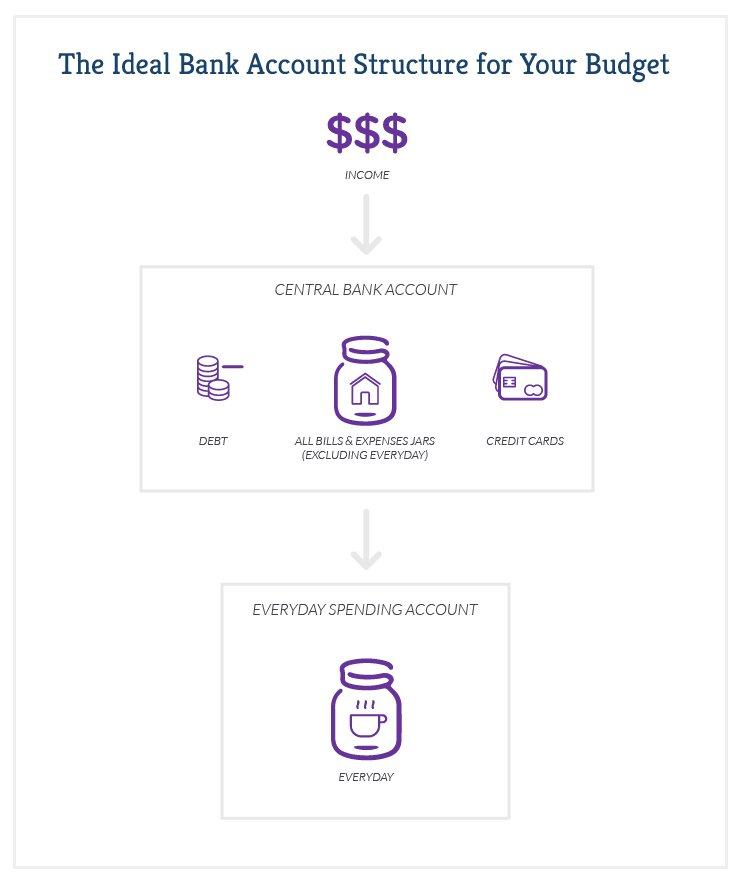

In this blog, I will outline the three-bank-account structure that we have been successfully using with our coaching clients for over 10 years. This ideal bank account structure supports the budgeting process and ensures that every bank account has a specific purpose.

The average individual or couple needs just three bank accounts and one credit (or debit) card to run the household budget.

The first and most important of these accounts is the:

Central Bank Account (or Bills Account)

This purposefully named account is the hub of your financial management system.

The central bank account should be used in the following way:

- All sources of household income are to flow into this account, ie. wages, bonuses, tips.

- With the exception of your ‘everyday jar’, all other money accumulating for future expenses is to be held in this account where it can earn some interest while remaining available to cover directs debit and periodical payments.

- From this account bills are paid – either via B-pay, direct debit, periodical payment or funds transfer.

- On the first day of every month your everyday allowance is transferred from this account to your ‘everyday account’ where cash or EFTPOS can be accessed for everyday spending.

- At the end of every month, surplus funds are transferred from this account to your high-interest savings or mortgage offset account.

- If you have a credit card, the balance owing on this card is paid from the ‘central account’ each month.

- You will need to be able to access funds in this account either by EFTPOS, debit or credit card as all but your ‘everyday spending’ will occur from this account.

Everyday Spending Account

Your everyday spending account is typically your standard everyday account with an ATM facility where you can access cash or use EFTPOS. The purpose of this account is pretty simple; it receives your monthly ‘Everyday Jar’ allowance on the first of every month, ie. the money allocated to groceries, petrol, parking, take away, entertainment, coffees, chocolate etc.

From this account, you pay for those items either by cash or EFTPOS but be aware – this is all you have for the month to spend on everyday expenses. If this money runs out its baked beans and mashed potatoes for the rest of the month! How To Save Money Everyday in Six Ways outlines some strategies for reducing these costs.

If it makes it easier to pace your spending, you can transfer the funds from your central account in two batches on the first and sixteenth of each month rather than in one lump at the beginning of each month.

The money is deliberately isolated in this bank account so that it forms a physical barrier to overspending in an area of spending that is typically the hardest to control. The golden rule for this account is simply this: you must not use your credit card or other accounts to fund everyday spending. This is all you have – you need to make it last the month.

Savings Account

The key focus for the savings account is high rates of interest, and no fees; we do not need functionality. High interest online bank accounts, or mortgage offset accounts are perfect for this.

Any funds that are not required to cover the accumulated funds in our jars, money owing on the credit card or our everyday allowance should be held in the savings account.

The savings account is the place we will hold our cash reserve, as well long funds for long-term savings goals.

Credit or Debit Cards

Our recommendation is of course that our members use debit cards in preference to credit cards, but that is a discussion best left for another day. A priority of the Grandma’s Jars system, once set up, will be to ensure that you always have the money to cover the balance owing on your credit card at the end of each month.

So there you have it – three bank accounts and one credit (or debit) card; no more, no less. This is the ideal bank account structure we have successfully used for the last 10-15 years. It’s not rocket science but it is amazing what a difference the ideal bank account structure will do to help keep your budgeting on track.